Founders

Our Firm

Commitment to Innovative Equity Research

Our objective is to achieve consistent outperformance

Prior to accepting assets in 1990, Bruce Jacobs and Ken Levy devoted over three years to researching market inefficiencies and analyzing the complex economic and behavioral factors underlying security returns. As part of this endeavor, they pioneered a proprietary process of “disentangling,” which evaluates numerous proprietary factors simultaneously, separating each potential source of return from the background noise created by other factors. This controls for cross-contamination of effects and results in "pure" return effects that are additive and can provide more reliable predictions of future stock price behavior than "naive" effects that result from analyzing one factor at a time.

The revolutionary findings resulting from this research led to the development of a unique multidimensional, dynamic approach to investing. Refined by over 35 years of research and experience, this approach allows for diversified portfolios across exposures to numerous potential opportunities, which can contribute to consistency of performance over time.

Groundbreaking Concepts

Introduced such concepts as the unique risks of leverage and leverage aversion into portfolio theory

The groundbreaking concepts that form the foundation of Jacobs and Levy’s investment philosophy and approach are articulated in numerous articles, which have received awards from the Financial Analysts Journal, Journal of Portfolio Management, and Journal of Investing. Many have become required reading for the CFA program and MBA courses.

Equity Management: The Art and Science of Modern Quantitative Investing, 2nd ed., published by McGraw-Hill, with a foreword by Nobel laureate Harry M. Markowitz, brings together 30 years of groundbreaking articles by Jacobs and Levy.

Equity Management contains what Harry Markowitz has called their seminal work on disentangling and integrated long-short portfolios, as well as articles about the growing popularity of factor investing, 130-30 and 150-50 long-short portfolios, portfolio optimization with short sales, optimizing portfolios for leverage-averse investors, market fragility and financial crises, and simulating security markets. The first edition of the book, Equity Management: Quantitative Analysis for Stock Selection, was translated into Chinese by China Machine Press.

Critically Acclaimed Insights

Research, at the intersection of theory and practice, offers forward-thinking, industry insiders' views

Bruce Jacobs and Ken Levy are the editors of Market Neutral Strategies, published by Wiley. This book provides industry insiders’ views of the implementation, risks, and benefits of long-short equity investing and other strategies.

How I Became a Quant: Insights from 25 of Wall Street’s Elite, also published by Wiley, profiles investment professionals at the forefront of the “quant revolution.” Jacobs and Levy contributed a chapter detailing the development of the firm and the Jacobs Levy investment philosophy.

Bruce Jacobs’s incisive analysis of modern capital ideas is evident in his critically acclaimed book, Capital Ideas and Market Realities, published by Blackwell. This work discusses the pitfalls of translating financial ideas into practice.

Bruce’s book Too Smart for Our Own Good: Ingenious Investment Strategies, Illusions of Safety, and Market Crashes, published by McGraw-Hill and translated into Chinese by China Machine Press, shows market crashes result from financial strategies that create an illusion of safety. He reveals how investment strategies that promise higher returns and protection from losses can end in greater risk for markets and the economy. This is especially true when they are characterized by opacity, complexity, leverage, and risk shifting.

Giving Forward

Contributing to the advancement of quantitative finance by fostering innovative research

Jacobs Levy Equity Management was a founding sponsor of the Research Foundation of the CFA Institute and of the Fischer Black Memorial Foundation.

In 1998, the firm founded the Bernstein Fabozzi/Jacobs Levy Awards to promote research excellence in the theory and practice of portfolio management, which annually recognize the best papers appearing in the Journal of Portfolio Management.

In 2011, in honor of the firm’s 25th anniversary, Jacobs and Levy founded the Jacobs Levy Equity Management Center for Quantitative Financial Research at The Wharton School and the Wharton-Jacobs Levy Prize for Quantitative Financial Innovation. The Jacobs Levy Equity Management Center for Quantitative Financial Research is dedicated to the advancement of quantitative finance, at the intersection of theory and practice, through the creation and dissemination of innovative knowledge. The Center also grants the biennial Wharton-Jacobs Levy Prize for Quantitative Financial Innovation to recognize those who have published articles that demonstrate outstanding quantitative research that have contributed to an innovation in the practice of finance.

Academic Engagement

In September 2011, in honor of Jacobs Levy Equity Management’s 25th anniversary, Bruce Jacobs and Ken Levy founded the Jacobs Levy Equity Management Center for Quantitative Financial Research at The Wharton School and the Wharton-Jacobs Levy Prize for Quantitative Financial Innovation.

Mission Statement

The Jacobs Levy Equity Management Center for Quantitative Financial Research is dedicated to the advancement of quantitative finance, at the intersection of theory and practice, through the creation and dissemination of innovative knowledge. The Jacobs Levy Center aims to enhance understanding of financial markets through the application of quantitative and statistical techniques and methods to such fields as asset management and security pricing, including the analysis of stocks, bonds and other instruments.

Wharton-Jacobs Levy Prize for Quantitative Financial Innovation

The Jacobs Levy Center also grants the biennial Wharton-Jacobs Levy Prize for Quantitative Financial Innovation to recognize one or more persons who have published peer-reviewed journal articles that demonstrate outstanding quantitative research that has contributed to a particular innovation in the practice of finance.

https://www.youtube.com/embed/5Fs254CxhmI

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 26, 2025

Conference on Frontiers in Quantitative Finance

New York, NY

September 26, 2025

https://www.youtube.com/embed/qAM38u21pkc

Presentation of the Wharton-Jacobs Levy Prize to Sanford “Sandy” J. Grossman

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 26, 2025

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 26, 2025

https://www.youtube.com/embed/iiGRyQufi6E

Highlights from the Tenth Jacobs Levy Center Conference

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

Philadelphia, PA

September 20, 2024

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

Philadelphia, PA

September 20, 2024

https://www.youtube.com/embed/rpdyJuqYfSw

Highlights from the Ninth Jacobs Levy Center Conference and Presentation of the Wharton-Jacobs Levy Prize to Albert S. “Pete” Kyle

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 22, 2023

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 22, 2023

https://www.youtube.com/embed/QbTBO-LFff8

Presentation of the Wharton-Jacobs Levy Prize to Albert S. "Pete" Kyle

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 22, 2023

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 22, 2023

https://www.youtube.com/embed/E9WWi88FAP4

Highlights from the Eighth Jacobs Levy Center Conference and Presentation of the Wharton-Jacobs Levy Prize to Narasimhan Jegadeesh and Sheridan Titman

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 16, 2022

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 16, 2022

https://www.youtube.com/embed/Oc-g00BBDRc

Presentation of the Wharton-Jacobs Levy Prize to Narasimhan Jegadeesh and Sheridan Titman

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 16, 2022

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 16, 2022

https://www.youtube.com/embed/PJZvTQOlxYY

Highlights from the Seventh Annual Jacobs Levy Center Conference and Presentation of the Wharton-Jacobs Levy Prize to Ray Ball and Philip Brown

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 27, 2019

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 27, 2019

https://www.youtube.com/embed/6ddQOKjqEE4

Presentation of the Wharton-Jacobs Levy Prize to Ray Ball and Philip Brown

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 27, 2019

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Frontiers in Quantitative Finance

New York, NY

September 27, 2019

https://youtube.com/embed/q7rPleZGGUQ

Highlights from the Sixth Annual Jacobs Levy Center Conference

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Financial Markets, Volatility, and Crises: A Decade Later

New York, NY

September 14, 2018

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Financial Markets, Volatility, and Crises: A Decade Later

New York, NY

September 14, 2018

https://www.youtube.com/embed/ovKQdJroljk

Bruce Jacobs Panelist – Impact of Financial Crises: Past, Present, and Future

Introductory Remarks: Michael Gibbons, Deputy Dean, The Wharton School

Vineer Bhansali, LongTail Alpha

Bruce Jacobs, Jacobs Levy Equity Management

Richard Lindsey, Windham Capital Management

Chester Spatt, Tepper School of Business at Carnegie Mellon University

Moderator: Richard Herring, The Wharton School

Jacobs Levy Equity Management Center for Quantitative Financial Research

Annual Conference

New York, NY

September 14, 2018

Introductory Remarks: Michael Gibbons, Deputy Dean, The Wharton School

Vineer Bhansali, LongTail Alpha

Bruce Jacobs, Jacobs Levy Equity Management

Richard Lindsey, Windham Capital Management

Chester Spatt, Tepper School of Business at Carnegie Mellon University

Moderator: Richard Herring, The Wharton School

Jacobs Levy Equity Management Center for Quantitative Financial Research

Annual Conference

New York, NY

September 14, 2018

https://www.youtube.com/embed/0RvgJuZViUU

Highlights from the Fifth Annual Jacobs Levy Center Conference and Presentation of the Wharton-Jacobs Levy Prize to Stephen A. Ross

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Quantitative Finance

New York, NY

September 15, 2017

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Quantitative Finance

New York, NY

September 15, 2017

https://www.youtube.com/embed/EHk_OblUEa8

Presentation of the Wharton-Jacobs Levy Prize to Steve Ross

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Quantitative Finance

New York, NY

September 15, 2017

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Quantitative Finance

New York, NY

September 15, 2017

https://www.youtube.com/embed/Gx24ecPizBk

Highlights from the Fourth Annual Jacobs Levy Center Conference and Presentation of the Wharton-Jacobs Levy Prize to William F. Sharpe

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 20, 2016

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 20, 2016

https://www.youtube.com/embed/_9Iwvo-1bIg

Presentation of the Wharton-Jacobs Levy Prize to Bill Sharpe

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 20, 2016

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 20, 2016

https://www.youtube.com/embed/Puq0JC35dw8

Highlights from the Third Annual Jacobs Levy Center Conference

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 1, 2015

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 1, 2015

https://www.youtube.com/embed/EwQyNRuLEnU

Bruce Jacobs Panelist – Is Smart Beta State of the Art?

Bruce Jacobs, Jacobs Levy Equity Management

Vitali Kalesnik, Research Affiliates

Jeremy Schwartz, WisdomTree Investments

Moderator: Thomas Mitchell, Marco Consulting

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 1, 2015

Bruce Jacobs, Jacobs Levy Equity Management

Vitali Kalesnik, Research Affiliates

Jeremy Schwartz, WisdomTree Investments

Moderator: Thomas Mitchell, Marco Consulting

Jacobs Levy Equity Management Center for Quantitative Financial Research

Spring Forum

New York, NY

May 1, 2015

https://www.youtube.com/embed/Mww6_1-Z-6Y

Highlights from the Second Annual Jacobs Levy Center Conference

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Quantitative Finance

The Wharton School

April 25, 2014

Jacobs Levy Equity Management Center for Quantitative Financial Research

Conference on Quantitative Finance

The Wharton School

April 25, 2014

https://www.youtube.com/embed/0k0kHw97Tv4

Highlights from the First Annual Jacobs Levy Center Conference and Presentation of the Wharton-Jacobs Levy Prize to Harry M. Markowitz

Jacobs Levy Equity Management Center for Quantitative Financial Research

Forum on Quantitative Finance

New York, NY

October 23, 2013

Jacobs Levy Equity Management Center for Quantitative Financial Research

Forum on Quantitative Finance

New York, NY

October 23, 2013

https://www.youtube.com/embed/Prs15tbCnMI

Leverage Aversion – A Third Dimension in Portfolio Theory

Bruce Jacobs and Ken Levy’s Keynote Presentation

Jacobs Levy Equity Management Center for Quantitative Financial Research

Forum on Quantitative Finance

New York, NY

October 23, 2013

“We've seen that there have been many catastrophes caused by excessive leverage, and that excessive leverage can give rise to systemic risk, market disruptions and economic crises.” — Bruce

“Just as investors are willing to sacrifice some return in order to reduce volatility risk, investors are willing to sacrifice some return in order to reduce leverage risk.” — Ken

Bruce Jacobs and Ken Levy’s Keynote Presentation

Jacobs Levy Equity Management Center for Quantitative Financial Research

Forum on Quantitative Finance

New York, NY

October 23, 2013

“We've seen that there have been many catastrophes caused by excessive leverage, and that excessive leverage can give rise to systemic risk, market disruptions and economic crises.” — Bruce

“Just as investors are willing to sacrifice some return in order to reduce volatility risk, investors are willing to sacrifice some return in order to reduce leverage risk.” — Ken

https://www.youtube.com/embed/Ge2i_3Pg3Hg

Presentation of the Wharton-Jacobs Levy Prize to Harry Markowitz

Jacobs Levy Equity Management Center for Quantitative Financial Research

Forum on Quantitative Finance

New York, NY

October 23, 2013

Jacobs Levy Equity Management Center for Quantitative Financial Research

Forum on Quantitative Finance

New York, NY

October 23, 2013

https://www.youtube.com/embed/OR26wfjBM5Y

Center Inauguration

Jacobs Levy Equity Management Center for Quantitative Financial Research

The Wharton School

September 7, 2011

Pictured (l-r): Dean Thomas, Bruce Jacobs, Ken Levy, Amy Gutmann

Jacobs Levy Equity Management Center for Quantitative Financial Research

The Wharton School

September 7, 2011

Pictured (l-r): Dean Thomas, Bruce Jacobs, Ken Levy, Amy Gutmann

Jacobs Levy Center News & Events

| Nov 11, 2025 |

The Lasting Impact of a 1976 Paper on Stock Information and Pricesread more |

Following the success of the Jacobs Levy Equity Management Center for Quantitative Financial Research at the Wharton School, in April 2020, Bruce Jacobs helped the School create a major in quantitative finance by establishing the Dr. Bruce I. Jacobs Professorship in Quantitative Finance and the Dr. Bruce I. Jacobs Scholars in Quantitative Finance. The professorship supports the appointment of faculty who are experts in quantitative finance, and the Scholars award is dedicated to exceptional quantitative finance majors entering their second year of the Wharton MBA program.

In a Bloomberg News article, Bruce comments that, “Now much of finance is quantitative, and it’s important that business leaders, regulators and the heads of Wall Street houses have a basic understanding of it.” Additionally, Bruce says in an article in Pensions & Investments, “Great progress has been achieved by the Jacobs Levy Center, Fellowship, and Prize at Wharton. Those successes and Wharton’s commitment to the future of finance inspired me to deepen my support of students and the faculty who will enrich future generations of leaders and the broader economy. I can think of no better time for this initiative as we face new economic, health, and markets issues that will shape the world economy for decades.”

Bruce is a pioneer and innovator in connecting academic research with investment management, and we are honored that he is making this bold new step in his immense ongoing support of the School. His new gift will attract and nurture talented students and faculty in quantitative finance to prepare a new generation of leaders in finance for the challenges we face today and in the future.

We've seen a lot of growth... There's been a lot of demand for these kinds of people who have very focused skills in these areas, data analytics, and finance.

Bruce Jacobs pictured with some of the 2024-2025 Jacobs Scholars on the University of Pennsylvania’s campus.

Bruce Jacobs pictured with some Jacobs Scholars at the 2023 Jacobs Levy Center conference in New York City.

-

Read about some of the inaugural Jacobs Scholars and why they choose to major in Quantitative Finance.

-

Learn more about the MBA Major in Quantitative Finance.

-

Bruce Jacobs was invited to be a member of the Industry Advisory Panel for the MBA Major in Quantitative Finance. Read about the Panel members here.

Statements made by individuals associated with the Wharton School are not recommendations of the advisory services of Jacobs Levy Equity Management or any of its employees. These individuals are not and have not been clients of the firm.

Quantitative Finance at Wharton News

| Apr 24, 2026 |

Reflections from a Graduating Jacobs Scholar: Q&A with Harry Kongread more |

| Aug 20, 2025 |

Reflections from a Jacobs Scholar: Q&A with Ksenia Bobrikread more |

| Jan 15, 2025 |

SEC Announces Departure of Chief Economist Jessica Wachterread more |

| May 22, 2024 |

Reflections from a Graduating Jacobs Scholar: Q&A with Zachary Longread more |

| Jun 06, 2023 |

Igniting Minds, Transforming Markets: Jacobs Scholars Impact at Wharton and Beyondread more |

| Apr 04, 2022 |

The Future is Financeread more |

| May 03, 2021 |

Jessica Wachter Named SEC Chief Economist and Director of the Division of Economic and Risk Analysisread more |

| Apr 20, 2020 |

Why Free-Lunch Strategies Cause Market Crashesread more |

| Apr 02, 2020 |

Wharton to Offer Quant MBA Major With $8 Million Alumnus Giftread more |

| Apr 02, 2020 |

Wharton Awarded $8 Million to Establish Quantitative Finance Majorread more |

| Apr 02, 2020 |

New Quantitative Finance Major and Dr. Bruce I. Jacobs Professorship and Scholars Mark New Chapter in Quantitative Finance Research and Education at the Wharton Schoolread more |

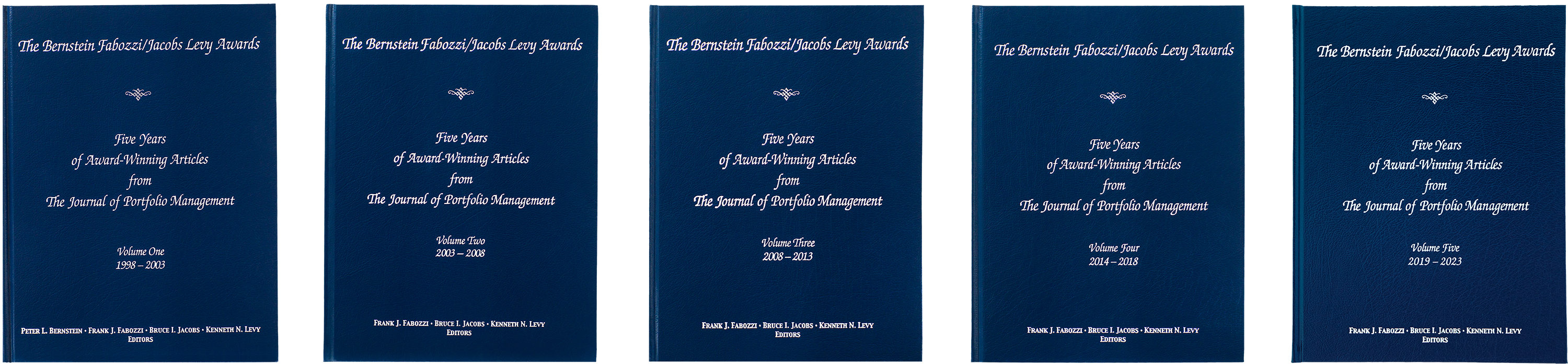

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of the Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management.

The Bernstein Fabozzi/Jacobs Levy Awards: Five Years of Award-Winning Articles from the Journal of Portfolio Management, Volumes One, Two, Three, Four, and Five.

The 20th Anniversary Celebration of the Bernstein Fabozzi/Jacobs Levy Awards

The 20th anniversary celebration of the Bernstein Fabozzi/Jacobs Levy Awards for the best articles in the Journal of Portfolio Management took place in New York City on November 21, 2019. The event celebrated the success of the Awards and commended its winners. Attendees included a host of key industry professionals and academics, and presenting were Bruce Jacobs, Ken Levy, Frank Fabozzi, Cliff Asness, Andrew Lo, and Meir Statman. The evening culminated with a presentation to the winners of the 20th Annual Bernstein Fabozzi/Jacobs Levy Awards.

https://www.youtube.com/embed/RVjHCBAwG18

Highlights from the 20th Anniversary Celebration of the Bernstein Fabozzi/Jacobs Levy Awards

New York, NY

November 21, 2019

New York, NY

November 21, 2019

https://www.youtube.com/embed/1pbZDMizaHk

20th Anniversary Celebration of the Bernstein Fabozzi/Jacobs Levy Awards

New York, NY

November 21, 2019

New York, NY

November 21, 2019

The 25th Anniversary Celebration of the Bernstein Fabozzi/Jacobs Levy Awards

Winners of Bernstein Fabozzi/Jacobs Levy Awards gathered in New York City on November 14, 2024 to celebrate 25 years of the Awards.

Pictured are:

Back row standing (l-r): Teun Draaisma, Tarun Gupta, Cliff Asness, Rob Arnott, Bruce Jacobs, Ken Levy, Marty Liebowitz, Harshdeep Ahluwalia, Andrew Weisman, Brett Hammond, Ankul Daga, Jennifer Bender

Front row sitting (l-r): Ron Kahn, Larry Siegel, Frank Fabozzi, Mark Anson

The First Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the First Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 1998 and ending with Summer 1999. As several articles tied for third outstanding award, there are two outstanding article awards granted this year. On the basis of voting by subscribers, the First Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Why Do Valuation Ratios Forecast Long-Run Equity Returns?

Thomas K. Phillips, Spring 1999

Outstanding Articles:

Long-Short Portfolio Management: An Integrated Approach

Bruce I. Jacobs, Kenneth N. Levy, and David Starer, Winter 1999

The History of Finance

Merton H. Miller, Summer 1999

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Second Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the Second Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beinning with Fall 1999 and ending with Summer 2000. Due to a tie vote, there are four outstanding article awards granted this year. On the basis of voting by subscribers, the Second Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

The Shrinking Equity Premium

Jeremy J. Siegel, Fall 1999

Outstanding Articles:

Performance Evaluation Using Conditional Alphas and BetasJon A. Christopherson, Wayne E. Ferson, and Andrew L. Turner, Fall 1999

The Investor Fear Gauge

Robert E. Whaley, Spring 2000

Optimizing Manager Structure and Budgeting Manager Risk

Barton Waring, Duane Whitney, John Pirone, and Charles Castille, Spring 2000

Beating Benchmarks

Steven Strongin, Melanie Petsch, and Greg Sharenow, Summer 2000

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Third Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Managment is pleased to announce the recipients of the Third Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2000 and ending with Summer 2001. Due to a tie vote, there are four outstanding articles awards granted this year. On the basis of voting by a selected panel, the Third Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

The Growth of Index Funds and the Pricing of Equity Securities

Burton G. Malkiel and Aleksander Radisich, Winter 2001

Outstanding Articles:

Value of Skill in Security Selection versus Asset Allocation in Credit Markets

Lev Dynkin, Jay Hyman, and Wei Wu, Fall 2000

Cognitive Biases in Market Forecasts

Kenneth L. Fisher and Meir Statman, Fall 2000

Why the Low Returns to Beta and Other Forms of Risk

Edward M. Miller, Winter 2001

The Death of the Risk Premium

Robert D. Arnott and Ronald J. Ryan, Spring 2001

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Fourth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the Fourth Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2001 and ending with Summer 2002. On the basis of voting by a selected panel,* the Fourth Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Do Hedge Funds Hedge?

Clifford S. Asness, Robert J. Krail, and John M. Liew, Fall 2001

Outstanding Articles:

Equity Index Funds Have Lost Their WayGary L. Gastineau, Winter 2002

The Small-Cap Alpha Myth

Richard M. Ennis and Michael D. Sebastian, Spring 2002

Informationless Investing and Hedge Fund Performance Measurement Bias

Andrew B. Weisman, Summer 2002

*The selection committee is a subset of the editorial advisory board. It excludes those boad members whose article is a candidate for the award. Frank Fabozzi, editor, and Peter Bernstein, consulting editor, are not on the selection committee. Articles authored by Frank Fabozzi or Peter Bernstein are not eligible for an award. The ballots are tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Fifth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the Fifth Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2002 and ending with Summer 2003. On the basis of voting by subscribers,* two articles tied for best article this year. As several articles tied for second outstanding award, there is one outstanding article award granted. The Fifth Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Articles:

Expected Returns on Stocks and Bonds

Antti Ilmanen, Winter 2003

The Hierarchy of Investment Choice

Mark Kritzman and Sébastien Page, Summer 2003

Outstanding Article:

A Critical Look at the Case for Hedge Funds

Richard M. Ennis and Michael D. Sebastian, Summer 2003

*The ballots are tallied by Institutional Investor Journals. Articles authored by Frank Fabozzi or Peter Bernstein are not eligible for an award.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Sixth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the Sixth Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2003 and ending with Summer 2004 as well as the special Real Estate issue from September 2003. On the basis of voting by subscribers,* the Sixth Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Fight the Fed Model

Clifford Asness, Fall 2003

Outstanding Articles:

Strategic versus Tactical Asset Allocation

Mark Anson, Winter 2004

Multiple Alpha Sources and Active Management

Eric H. Sorensen, Edward Qian, Robert Schoen, and Ronald Hua, Winter 2004

Liability-Relative Investing

M. Barton Waring, Summer 2004

*Articles authored by Frank Fabozzi or Peter Bernstein were not eligible for an award. Authors were not permitted to vote for thier own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Seventh Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the Seventh Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2004 and ending with Summer 2005 as well as the 30th Anniversary issue. On the basis of voting by subscribers,* the Seventh Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

The Active Risk Puzzle

Robert Litterman, 30th Anniversary Issue

Outstanding Articles:

The Adaptive Markets Hypothesis

Andrew W. Lo, 30th Anniversary Issue

An Alternative Future, Part II

Clifford Asness, Fall 2004

Five Myths of Active Portfolio Management

Jonathan B. Berk, Spring 2005

*Articles authored by Frank Fabozzi or Peter Bernstein were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Eighth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the Eighth Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2005 and ending with Summer 2006 as well as the special Real Estate issue from September 2005. On the basis of voting by subscribers,* the Eighth Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Five Myths About Fees

Ronald N. Kahn, Matthew H. Scanlan, Laurence B. Siegel, Spring 2006

Outstanding Articles:

A Factor Approach to Asset Allocation

Roger G. Clarke, Harindra de Silva, Robert Murdock, Fall 2005

Attribution

Richard Grinold, Winter 2006

Are Optimizers Error Maximizers?

Mark Kritzman, Summer 2006

*Articles authored by Frank Fabozzi or Peter Bernstein were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Ninth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Award was established in 1999 to honor the Editors’ 25 years of extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the Eighth Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2006 and ending with Summer 2007. On the basis of voting by subscribers,* the Ninth Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Gathering Implicit Alphas in a Beta World

Martin Leibowitz and Anthony Bova, Spring 2007

Outstanding Articles:

Minimum-Variance Portfolios in the U.S. Equity Market

Roger Clarke, Harindra de Silva, and Steven Thorley, Fall 2006

The Relative Importance of Asset Allocation and Security Selection

Kodjovi Assoé, Jean-François L’Her, and Jean-François Plante, Fall 2006

Execution Risk

Robert Engle and Robert Ferstenberg, Winter 2007

*Articles authored by Frank Fabozzi or Peter Bernstein were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Tenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the Tenth Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2007 and ending with Summer 2008 as well as the special Real Estate issue from September 2007. On the basis of voting by subscribers,* the Tenth Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Dynamic Portfolio Analysis

Richard Grinold, Fall 2007

Outstanding Articles:

Information Horizon, Portfolio Turnover, and Optimal Alpha Models

Edward Qian, Eric H. Sorensen, and Ronald Hua, Fall 2007

A Question So Important That It Should Be Hard to Think About Anything Else

John C. Bogle, Winter 2008

130/30: The New Long-Only

Andrew W. Lo and Pankaj N. Patel, Winter 2008

*Articles authored by Frank Fabozzi or Peter Bernstein were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Eleventh Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 11th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2008 and ending with Summer 2009. On the basis of voting by subscribers,* the 11th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Understanding the VIX

Robert E. Whaley, Spring 2009

Outstanding Articles:

Alternatives and Liquidity: Will Spending and Capital Calls Eat Your "Modern" Portfolio?

Laurence B. Siegel, Fall 2008

Luck, Skill, and Investment Performance

Bradford Cornell, Winter 2009

The Black-Litterman Model for Active Portfolio Management

Alexandre S. Da Silva, Wai Lee, and Bobby Pornrojnangkoo, Winter 2009

*Articles authored by Frank Fabozzi or Peter Bernstein were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twelfth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 12th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Fall 2009 and ending with Fall 2010 as well as the special Real Estate issue from September 2009. On the basis of voting by subscribers,* the 12th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Active Portfolio Management and Positive Alphas: Fact or Fantasy?

Robert A.Jarrow, Summer 2010

Outstanding Articles:

The Fiduciary Principle: No Man Can Serve Two Masters

John C.Bogle, Fall 2009

The Myth of Diversification

David B Chua, Mark Kritzman, and Sébastien Page, Fall 2009

Crisis and Innovation

Robert J. Shiller, Spring 2010

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Thirteenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 13th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Winter 2011 through Fall 2011 as well as the Spring Real Estate issue from September 2011. On the basis of voting by subscribers,* the 13th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Risk-Based Asset Allocation: A New Answer to an Old Question?

Wai Lee, Summer 2011

Outstanding Articles:

Minimum-Variance Portfolio Composition

Roger Clarke, Harindra de Silva, and Steven Thorley, Winter 2011

The Description of Portfolios

Richard Grinold, Winter 2011

Principal Components as a Measure of Systemic Risk

Mark Kritzman, Yuanzhen Li, Sébastien Page, and Roberto Rigobon, Summer 2011

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Fourteenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 14th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Winter 2012 through Fall 2012. On the basis of voting by subscribers,* the 14th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

The Death of Diversification Has Been Greatly Exaggerated

Antti Ilmanen and Jared Kizer, Spring 2012

Outstanding Articles:

The Norway Model

David Chambers, Elroy Dimson, and Antti Ilmanen, Winter 2012

Risk On / Risk Off

Wai Lee, Spring 2012

Diversification Return and Leveraged Portfolios

Edward Qian, Spring 2012

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Fifteenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 15th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Winter 2013 through Fall 2013, as well as the Special Real Estate issue from September 2013. On the basis of voting by subscribers,* two articles tied for Best, and there was also a tie for Outstanding this year. The 15th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Articles:

Volatility, Correlation, and Diversification in a Multi-Factor World

Richard Roll, Winter 2013

The Devil in HML's Details

Clifford Asness and Andrea Frazzini, Summer 2013

Outstanding Articles:

Diversification Across Time

Ian Ayres and Barry Nalebuff, Winter 2013

Liquidity and Portfolio Choice: A United Approach

Will Kinlaw, Mark Kritzman, and David Turkington, Winter 2013

The Surprising Alpha from Malkiel's Monkey and Upside-Down Strategies

Robert D. Arnott, Jason Hsu, Vitali Kalesnik, and Phil Tindall, Summer 2013

Risk Disparity

Mark Kritzman, Fall 2013

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Sixteenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 16th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Winter 2014 through Fall 2014, as well as the Special 40th Anniversary issue from September 2014. Due to a tie vote, there are four outstanding article awards granted this year. On the basis of voting by subscribers,* the 16th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Evaluating Trading Strategies

Campbell R. Harvey and Yan Liu, 40th Anniversary Issue, September 2014

Outstanding Articles:

Can Alpha Be Captured by Risk Premia?

Jennifer Bender, P. Brett Hammond, and William Mok, Winter 2014

A Study of Low-Volatility Portfolio Construction Methods

Tzee-man Chow, Jason C. Hsu, Li-lan Kuo, and Feifei Li, 40th Anniversary Issue, September 2014

The Divergence of High- and Low-Frequency Estimation: Causes and Consequences

William Kinlaw, Mark Kritzman, and David Turkington, 40th Anniversary Issue, September 2014

Tesla: Anatomy of a Run-Up

Bradford Cornell and Aswath Damodaran, Fall 2014

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Seventeenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 17th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Winter 2015 through Fall 2015, as well as the Special China issue from January 2015 and Real Estate issue from September 2015. On the basis of voting by subscribers,* the 17th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Backtesting

Campbell R. Harvey and Yan Liu, Fall 2015

Outstanding Articles:

A Penalty Cost Approach to Strategic Asset Allocation with Illiquid Asset Classes

Mark Hayes, James A. Primbs, and Ben Chiquoine, Winter 2015

The Divergence of High- and Low-Frequency Estimation: Implications for Performance Measurement

Will Kinlaw, Mark Kritzman, and David Turkington, Spring 2015

Fact, Fiction, and Value Investing

Clifford Asness, Andrea Frazzini, Ronen Israel, and Tobias Moskowitz, Fall 2015

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Eighteenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for Best Article and $1,000 prizes for each of three Outstanding Articles.

The Journal of Portfolio Management is pleased to announce the recipients of the 18th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the sequence of four issues beginning with Winter 2016 through Fall 2016, as well as the Special Quantitative Equity Strategies issue from May 2016. On the basis of voting by subscribers,* the 18th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

What Is an Index?

Andrew W. Lo, Winter 2016

Outstanding Articles:

Stability-Adjusted Portfolios

Mark Kritzman and David Turkington, Special QES Issue 2016

Alpha Signals, Smart Beta, and Factor Model Alignment

Terry Marsh and Paul Pfleiderer, Special QES Issue 2016

David and Goliath: Who Wins the Quantitative Battle?

John C. Bogle, Fall 2016

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Nineteenth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for the Best Article and $1,000 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 19th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in four regular issues beginning with Winter 2017 through Fall 2017, as well as the Special Quantitative Strategies issue from March 2017 and the Real Estate issue from September 2017. On the basis of voting by subscribers,* the 19th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

King of the Mountain: The Shiller P/E and Macroeconomic Conditions

Robert D. Arnott, Denis B. Chaves, and Tzee-man Chow, Fall 2017

Outstanding Articles:

Factor-Based Investing: The Long-Term Evidence

Elroy Dimson, Paul Marsh, and Mike Staunton, Special Quant Issue 2017

Does Past Performance Matter in Investment Manager Selection?

Bradford Cornell, Jason Hsu, and David Nanigian, Summer 2017

Man vs. Machine: Comparing Discretionary and Systematic Hedge Fund Performance

Campbell R. Harvey, Sandy Rattray, Andrew Sinclair, and Otto Van Hemert, Summer 2017

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles.

The ballots were tallied by Institutional Investor Journals.

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles.

The ballots were tallied by Institutional Investor Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twentieth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $2,500 prize for the Best Article and $1,000 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 20th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in four regular issues beginning with Winter 2018 through Fall 2018, as well as the Multi-Asset Strategies issue from December 2017, the Quantitative Strategies issue from March 2018, and the Stephen A. Ross issue from June 2018. On the basis of voting by subscribers,* the 20th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Behavioral Efficient Markets

Meir Statman, Winter 2018

Outstanding Articles:

Proverbial Baskets Are Uncorrelated Risk Factors! A Factor-Based Framework for Measuring and Managing Diversification in Multi-Asset Investment Solutions

Lionel Martellini and Vincent Milhau, Multi-Asset Strategies Issue, December 2017

Buyback Derangement Syndrome

Clifford Asness, Todd Hazelkorn, and Scott Richardson, Spring 2018

The Impact of Volatility Targeting

Campbell R. Harvey, Edward Hoyle, Russell Korgaonkar, Sandy Rattray, Matthew Sargaison, and Otto Van Hemert, Fall 2018

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles.

The ballots were tallied by Institutional Portfolio Research Journals.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twenty-First Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $5,000 prize for Best Article and $2,500 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 21st Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in the four regular issues from April 2019 through November 2019, as well as the Multi-Asset-Strategies, Quantitative Strategies, and Real Estate special issues. On the basis of voting by subscribers,* the 21st Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Factor Momentum Everywhere

Tarun Gupta and Bryan Kelly, Quantitative Strategies Special Issue 2019

Outstanding Articles:

Asset Allocation vs. Factor Allocation—Can We Build a Unified Method?

Jennifer Bender, Jerry Le Sun, and Ric Thomas, Multi-Asset Strategies Special Issue 2019

Extending Fama-French Factors to Corporate Bond Markets

Demir Bektić, Josef-Stefan Wenzler, Michael Wegener, Dirk Schiereck, and Timo Spielmann, Quantitative Strategies Special Issue 2019

Alice's Adventures in Factorland: Three Blunders That Plague Factor Investing

Rob Arnott, Campbell R. Harvey, Vitali Kalesnik, and Juhani Linnainmaa, April 2019

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Portfolio Management Research.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twenty-Second Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $5,000 prize for Best Article and $2,500 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 22nd Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in 2020. This year, two articles tied for Best Article. As several articles tied for the third Outstanding award, two articles were granted Outstanding Article. On the basis of voting by subscribers,* the 22nd Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Articles:

Alpha vs. Alpha: Selection, Timing, and Factor Exposures from Different Factor Models

Ananth Madhavan, Aleksander Sobczyk, and Andrew Ang, Fund Manager Selection 2020

Divergent ESG Ratings

Elroy Dimson, Paul Marsh, and Mike Staunton, November 2020

Outstanding Articles:

Smart Beta: The Good, the Bad, and the Muddy

James White and Victor Haghani, March 2020

Portfolio Optimization with Active, Passive, and Factors: Removing the Ad Hoc Step

Roger Aliaga-Diaz, Giulio Renzi-Ricci, Ankul Daga, and Harshdeep Ahluwalia, March 2020

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. The ballots were tallied by Pageant Media, Ltd.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twenty-Third Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $5,000 prize for Best Article and $2,500 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 23rd Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in 2021. On the basis of voting by subscribers,* the 23rd Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

The Best Strategies for Inflationary Times

Henry Neville, Teun Draaisma, Ben Funnell, Campbell R. Harvey, and Otto Van Hemert, August 2021

Outstanding Articles:

Is (Systematic) Value Investing Dead?

Ronen Israel, Kristoffer Laursen, and Scott Richardson, Quantitative Special Issue 2021

Deep Value

Cliff Asness, John Liew, Lasse Heje Pedersen, and Ashwin Thapar, Multi-Asset Special Issue 2021

The Myth of Diversification Reconsidered

William Kinlaw, Mark Kritzman, Sébastien Page, and David Turkington, August 2021

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. Subscribers were not permitted to vote for articles whose author(s) are from their organization. The ballots were tallied by Portfolio Management Research.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twenty-Fourth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $5,000 prize for Best Article and $2,500 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 24th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in 2022. On the basis of voting by subscribers,* the 24th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Quantifying Long-Term Market Impact

Campbell R. Harvey, Anthony Ledford, Emidio Sciulli, Philipp Ustinov, and Stefan Zohren, February 2022

Outstanding Articles:

The Covariance Structure between Liquid and Illiquid Assets

Marielle de Jong, February 2022

Intangibles: The Missing Ingredient in Book Value

Feifei Li, February 2022

Corporate Bonds and Climate Change Risk

Afsaneh Mastouri, Rohit Mendiratta, and Guido Giese, Novel Risks 2022

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. Subscribers were not permitted to vote for articles whose author(s) are from their organization. The ballots were tallied by Portfolio Management Research.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twenty-Fifth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $5,000 prize for Best Article and $2,500 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 25th Annual Bernstein Fabozzi/Jacobs Levy Awards for articles appearing in 2023. On the basis of voting by subscribers,* the 25th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Fact, Fiction, and Factor Investing

Michele Aghassi, Cliff Asness, Charles Fattouche, and Tobias J. Moskowitz, Quantitative Special Issue 2023

Outstanding Articles:

Where Are the Factors in Factor Investing?

Marcos López de Prado, April 2023

From ELIZA to ChatGPT: The Evolution of Natural Language Processing and Financial Applications

Andrew W. Lo, Manish Singh, and ChatGPT, July 2023

Compound Tail Risk

Robert F. Engle, Novel Risks Special Issue 2023

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. Subscribers were not permitted to vote for articles whose author(s) are from their organization. The ballots were tallied by Portfolio Management Research.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twenty-Sixth Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $10,000 prize for Best Article and $5,000 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 26th Annual Bernstein Fabozzi/Jacobs Levy Awards for research articles appearing in 2024. On the basis of voting by subscribers,* the 26th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Factor Zoo (.zip)

Alexander Swade, Matthias X. Hanauer, Harald Lohre, and David Blitz, Quantitative Special Issue 2024

Outstanding Articles:

Dynamic Asset Allocation Using Machine Learning: Seeing the Forest for the Trees

Christian Mueller-Glissmann and Andrea Ferrario, Multi-Asset Special Issue 2024

Do Alternative Risk Premia Diversify? New Evidence for the Post-Pandemic Era

Antti Suhonen and Kari Vatanen, Multi-Asset Special Issue 2024

The Less-Efficient-Market Hypothesis

Clifford Asness, 50th Anniversary Special Issue 2024

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. Subscribers were not permitted to vote for articles whose author(s) are from their organization. The ballots were tallied by Portfolio Management Research.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

The Twenty-Seventh Annual Bernstein Fabozzi/Jacobs Levy Awards

The Bernstein Fabozzi/Jacobs Levy Awards were established in 1999, on the 25th anniversary of The Journal of Portfolio Management, to honor Editors Peter Bernstein and Frank Fabozzi for their extraordinary contributions to the field of finance and to promote research excellence in the theory and practice of portfolio management. The annual awards, co-founded and generously funded by Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management, consist of a $10,000 prize for Best Article and $5,000 prizes for each of three Outstanding Articles.The Journal of Portfolio Management is pleased to announce the recipients of the 27th Annual Bernstein Fabozzi/Jacobs Levy Awards for research articles appearing in 2025. On the basis of voting by subscribers,* the 27th Annual Bernstein Fabozzi/Jacobs Levy Awards are presented to:

Best Article:

Return to Active Equity Management

Eric H. Sorensen, Future of Asset Management 2025

Outstanding Articles:

How Misunderstanding Factor Models Set Unreasonable Expectations for Smart Beta

Bruce I. Jacobs, Kenneth N. Levy, and Sangwoo Lee, Quantitative Special Issue 2025

Agent Investing: A Constructive Approach

Jarrod Wilcox, William Zieff, and Stephen Satchell, February 2025

Strategic Asset Allocation with Alternative Investments: An Integrated Approach

Alexander Rudin and Daniel Farley, August 2025

*Articles authored by Frank Fabozzi were not eligible for an award. Authors were not permitted to vote for their own articles. Subscribers were not permitted to vote for articles whose author(s) are from their organization. The ballots were tallied by Portfolio Management Research.

Additional Bernstein Fabozzi/Jacobs Levy Awards:

Philanthropy and Community

We want to make a real difference in people’s lives by encouraging research and activities that have the potential to improve the financial, physical, and cultural well-being of the members of our industry and our larger community.

for Quantitative Financial Research

and Research Program

Innovation and a thirst for knowledge have driven our own breakthroughs in quantitative investing. Hoping to inspire both, we established the Jacobs Levy Equity Management Center for Quantitative Financial Research at the Wharton School of the University of Pennsylvania in September 2011. The Jacobs Levy Center provides research grants and fellowships and aims to motivate research leading to practical applications that can improve everyone’s financial well-being. Following the success of the Jacobs Levy Center, in April 2020 Bruce Jacobs helped the Wharton School create a major in quantitative finance and established the Dr. Bruce I. Jacobs Professorship in Quantitative Finance and the Dr. Bruce I. Jacobs Scholars in Quantitative Finance. The professorship supports the appointment of faculty who are experts in quantitative finance, and the Scholars award is given to exceptional quantitative finance majors entering their second year of the Wharton MBA program. We also support the CFA Institute Research Foundation and the International Association for Quantitative Finance’s Fischer Black Memorial Foundation.

Our desire to support innovation and its application also motivated our gift to create the Jacobs Levy Genomic Medicine and Research Program. Affiliated with Atlantic Health System, the program integrates genetic medicine into everyday practice, enabling physicians to diagnose and design highly personalized treatments for rare diseases as well as common conditions. The program has expanded to include clinical trials, which will help advance medical breakthroughs. The American Cancer Society awarded Jacobs Levy its Jody A. Morrow Humanitarian Award in 2014 for our role in creating this innovative program.

We are also pleased to support a number of New Jersey-based cultural institutions, including a program of the New Jersey Performing Arts Center that sponsors a resident teacher to bring music, dance, and theater education to underserved communities.

We are proud to support many organizations that foster education opportunities and champion diversity. A few examples are Roots & Wings, which provides housing, educational support, counseling, and life skills to young adults who graduate from the foster care system; Sponsors for Educational Opportunities, which offers academic programs to help low-income high school students reach college and earn degrees; A Better Chance; Braven; and the Children’s Scholarship Fund.

We will continue to seek opportunities to fulfill our role as a responsible corporate citizen and make a positive impact in our local and business communities and around the globe.

“We are very grateful to Bruce Jacobs and Ken Levy for their foresight and generosity to the community they live in. We know this program [Jacobs Levy Genomic Medicine and Research] will have a positive impact on the community we serve.”

— David Shulkin, M.D., President, Morristown Medical Center, and Vice President, Atlantic Health System

“Since the launch of The Miracle Project program for children on the autism spectrum and with other special needs, Bruce Jacobs and Ken Levy of Jacobs Levy Equity Management provided the seed money and have continued to be avid proponents providing major lead support annually for The Miracle Project program.”

— Allison Larena, President and CEO, Mayo Performing Arts Center

“Bruce and Ken’s generosity significantly impacts the Foundation’s support of our community’s human services and cultural non-profits. We are most grateful.”

— Andrew Boles, Board President, Park Avenue Foundation

“The establishment of the Jacobs Levy Equity Management Center for Quantitative Financial Research is an extremely significant event for the Wharton School and for the field as a whole.”

— Thomas Robertson, Dean, The Wharton School

“Bruce is a pioneer and innovator in connecting academic research with investment management, and we are honored that he is making this bold new step in his immense ongoing support of the School. His new gift will attract and nurture talented students and faculty in quantitative finance to prepare a new generation of leaders in finance for the challenges we face today and in the future.”

— Geoff Garrett, Dean, The Wharton School

https://www.youtube.com/embed/CjZuEo2qsB4

Bruce Jacobs's Acceptance Speech

Jacobs Levy Equity Management Awarded the Jody A. Morrow Humanitarian Award

American Cancer Society's Diamond Ball

November 15, 2014

Jacobs Levy Equity Management Awarded the Jody A. Morrow Humanitarian Award

American Cancer Society's Diamond Ball

November 15, 2014

https://www.youtube.com/embed/Jo6ddL9n-Co

Bruce Jacobs and Ken Levy’s Acceptance Speech

Jacobs Levy Equity Management Awarded the John T. Cunningham Award

Mayo Performing Arts Center’s Starlight Ball

November 14, 2015

Jacobs Levy Equity Management Awarded the John T. Cunningham Award

Mayo Performing Arts Center’s Starlight Ball

November 14, 2015

|

Jacobs Levy Equity Management |  |

© 2026 Jacobs Levy Equity Management. All rights reserved.